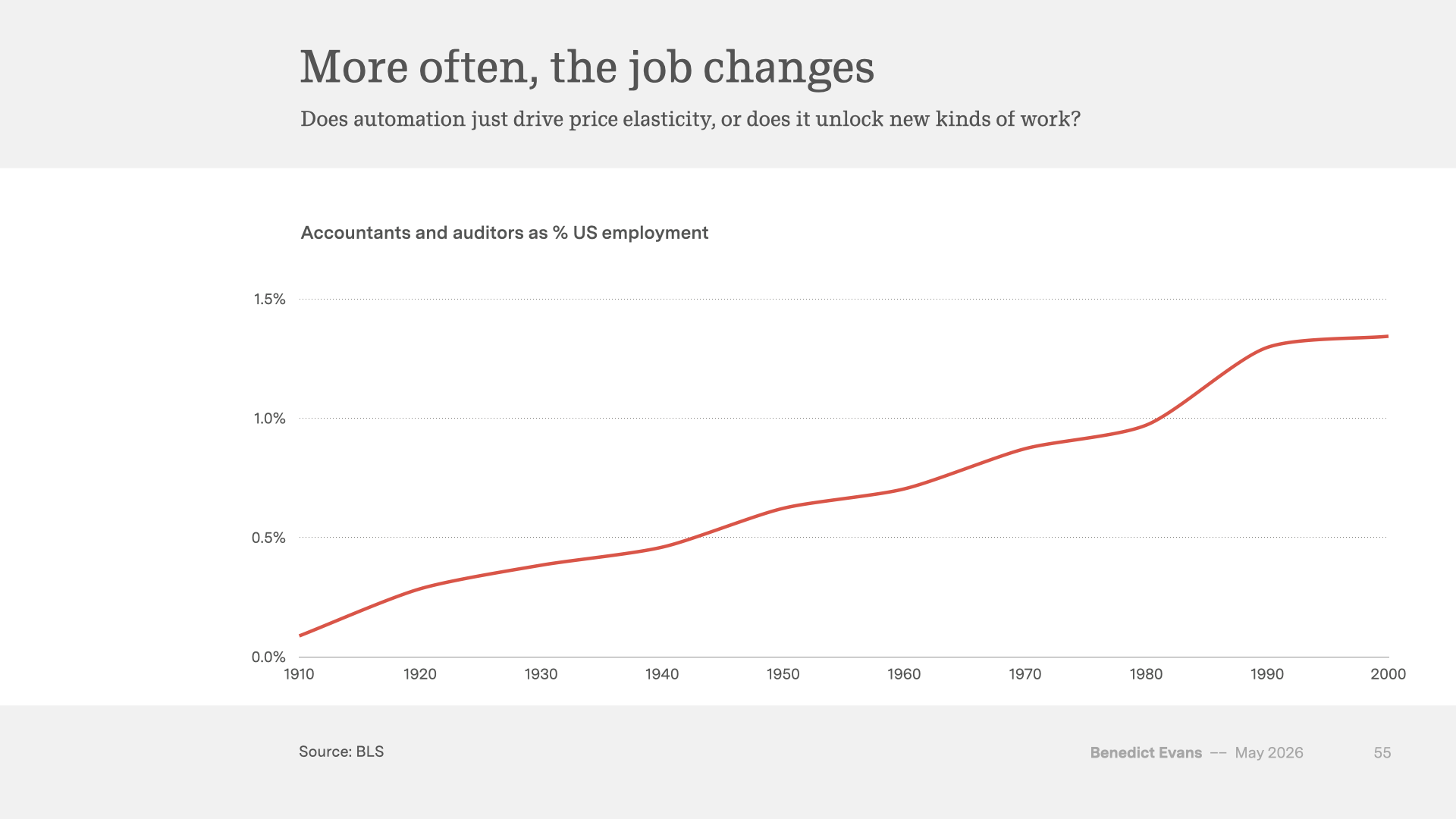

Predicting AI job exposure

Many people would like to analyse which jobs, companies and industries are most exposed to AI, and assign scores, build charts, and map that against the progress of LLMs. I think this is mostly impossible: you don’t know how the jobs will change, you don’t know what else will change around this, and you can’t measure work like that anyway.

Read More

How will OpenAI compete?

OpenAI has some big questions. It doesn’t have unique tech. It has a big user base, but with limited engagement and stickiness and no network effect. The incumbents have matched the tech and are leveraging their product and distribution. And a lot of the value and leverage will come from new experiences that haven’t been invented yet, and it can’t invent all of those itself. What’s the plan?

Read More

AI, networks and Mechanical Turks

How far do LLMs give us a step change in how good a search and recommendation system can be? Do they let you build one without needing a vast user base of your own?

Read More

AI metrics

With every platform shift, we want to measure the growth but we’re confused about what to measure. That’s partly a problem of data and definitions, but it’s really a question about what this is going to be.

Read More

GenAI’s adoption puzzle

Generative AI chatbots might be a life-changing transformation in the nature of computing, that can replace all software, but so far, most of its users only pick it up every week or two, and far fewer have made it part of their lives. Is that a time problem or a product problem?

Read More

What kind of disruption?

Software ate the world. Uber and Airbnb didn’t sell software - they disrupted and redefined markets. But what kind of disruption are we talking about ?

Read More

Apple innovation and execution

It matters that Apple’s new Siri will be late, and it matters more that Apple didn’t realise. Is it more than that?

Read More

The Deep Research problem

OpenAI’s Deep Research is built for me, and I can’t use it. It’s another amazing demo, until it breaks. But it breaks in really interesting ways.

Read More

Are better models better?

Every week there’s a better AI model that gives better answers. But a lot of questions don’t have better answers, only ‘right’ answers, and these models can’t do that. So what does ‘better’ mean, how do we manage these things, and should we change what we expect from computers?

Read More

Competing in search

A quarter century after ‘don't be evil’ a judge has found that Google is abusing its monopoly in search. But no-one knows what happens next, and whether this ruling will change anything. Will Apple build a search engine? Will ChatGPT change search? Does it matter?

Read More