The end of the beginning

The mobile revolution (or whatever you want to call it) is well underway. Smartphones and tablets running iOS and Android will outsell PCs by more than 2:1 in 2012, and there will be 1bn of these devices in use by the end of the year, compared to around 1.5-1.6bn PCs.

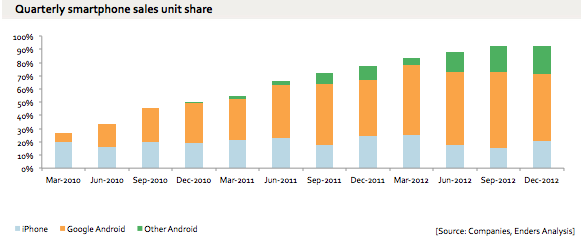

The sales of these devices, as anyone paying attention knows, are totally dominated by platforms from Apple and Google: between them the iPhone and Android smartphones now make up at least 90% of all smartphone sales. Inter alia, this means that Microsoft's share of connected device sales has dropped from around 90% at the beginning of 2009 to perhaps 30% at the end of 2012.

(Note: this chart adds forecast Q4 2012 sales to capture the beginning of the next Apple product cycle)

This is not the end of the story, though: global mobile phone sales will be perhaps 1.6bn in 2012, and iOS and Android smartphones were 'only' 625m or so of that. There is more growth to come. Of course, not all (by any means) of the people buying phones can afford smartphones, but Android phones are now dropping below $45 at wholesale, so a very large proportion of those phone sales will convert to Android. If nothing changes (a very dangerous assumption), it seems quite likely that Android sales in a year or two will pass 1bn units a year. If Apple does nothing about it.

What is 'Android'?

But what do we mean when we say 'Android'? Android does not fit historical analogies. Hugh Trevor-Roper is supposed to have said that 'history teaches us nothing except that something will happen', and this applies pretty well to tech: this is so young and so fast-changing an industry that drawing parallels is more misleading than helpful. Android is not the 'dominant' Windows crushing Apple in the 1990s, nor the 'fragmented' Linux, nor the 'not actually used as a smartphone' Symbian: it has things in common with all of these but it is itself, and has some unique characteristics that make it look very different from all of these and very different from iOS.

In particular, a third to a quarter of the 'Android' base is in China and cut off from all Google services (this is the 'Other Android' in the first chart). (link)

Most fundamentally, there is a very strong strain of 'self selection' running through the user base of these devices. The iPhone is a $650 device, more than almost all Android phones, which is manifested in either a more expensive contract or a higher sticker price, or both (though the US market structure tends to conceal this). Conversely most Android volume is at prices below $300 - the flagship Samsung Galaxy SIII made up no more than 15-20% of total Android sales in the last 6 months.

It ought not to be contentious to point out that people buying $300 smartphones will probably use them differently from people buying $650 smartphones: people buying those $45 Androids will behave differently again. A Kenyan or Indian saving up to buy a $45 Android probably badly wants the internet, but a Frenchman buying a €100 smartphone has probably decided that he doesn't.

In other words, Apple has 20-30% of the market by volume, but it is the top 20-30%. Google 'has' the rest, but has only a very tenuous connection to large parts of it, and another large proportion is likely to be worth little or nothing for a long time. Roll on uncertainty (link): everything will change, again, in the next year.