The end of a mobile wave; the Dell of mobile

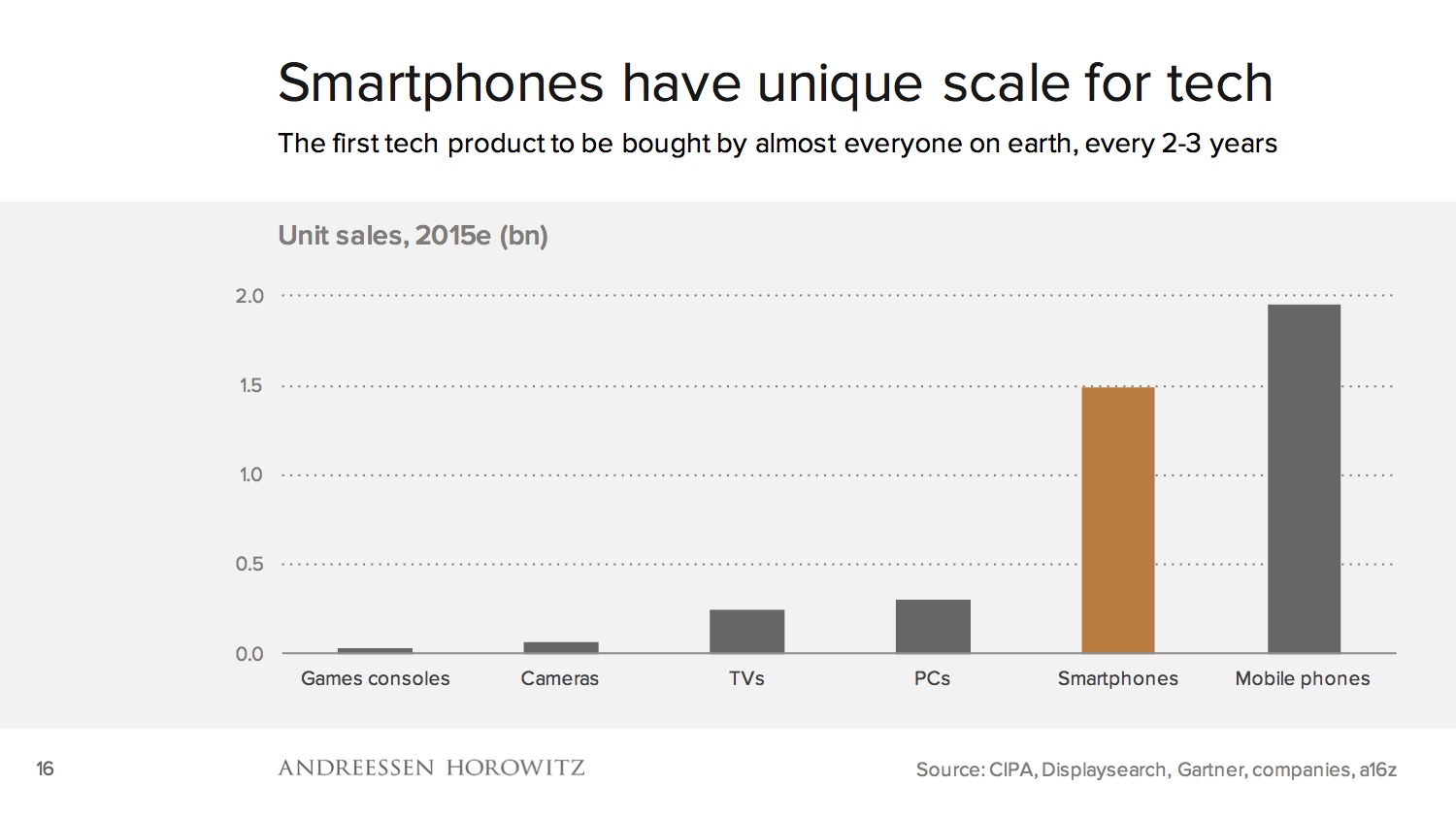

The mobile phone industry has had two waves - first voice and SMS and then the smartphone. The voice wave has taken it from zero to 5 billion people on earth with a mobile phone, and now close to 2 billion mobile phones are sold every year. In parallel, starting 9 years ago, the smartphone wave converted a larger and larger percentage of those phone sales to smartphones.

And since smartphones could be sold for higher average prices than feature phones, revenue grew even faster than unit sales. This was a great multiplier for the right companies - smartphones were a growing percentage of growing phone sales at growing prices.

All of this is now reaching an end - the wave is almost over.

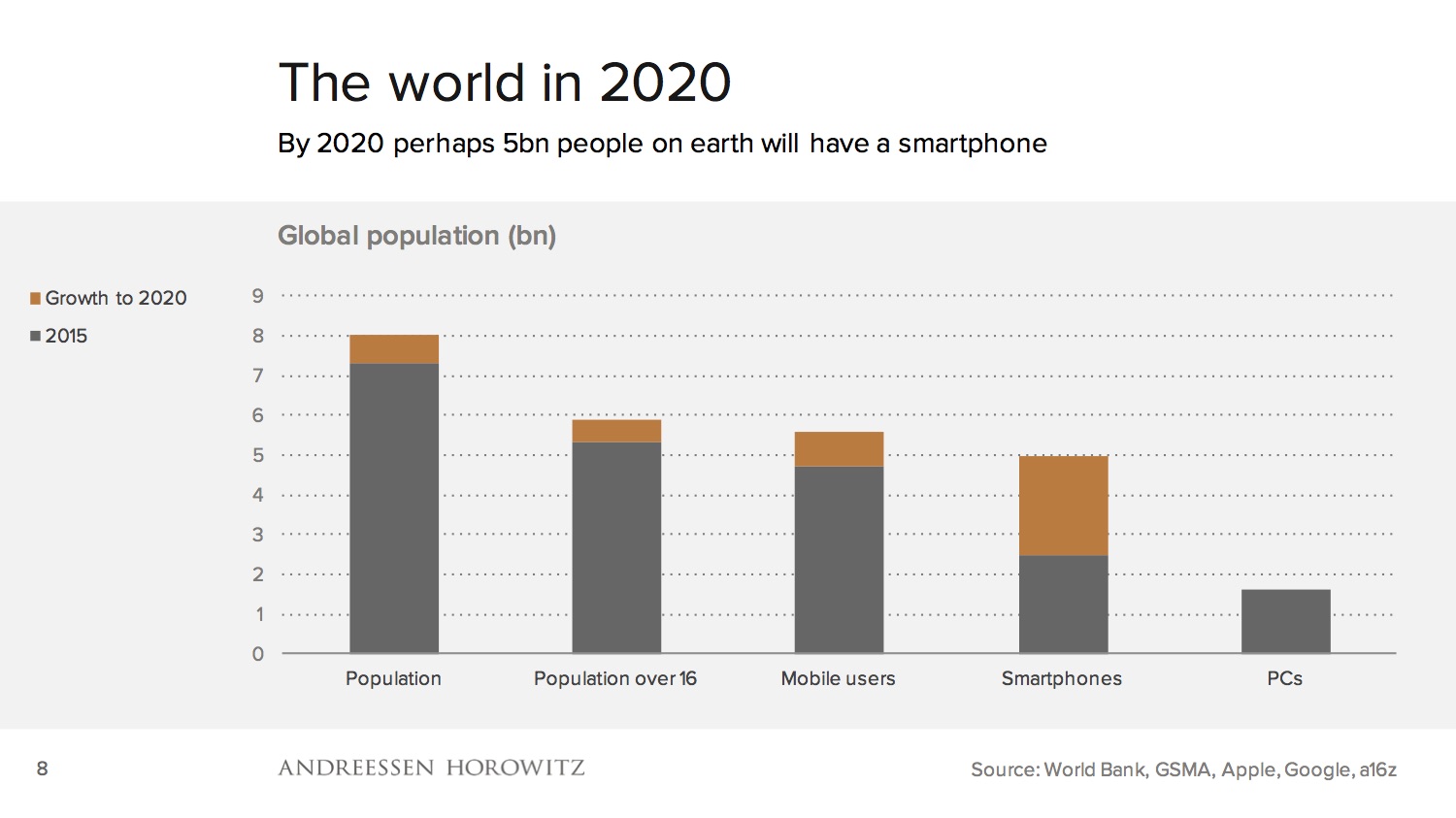

By 2020 there'll be 6bn adults on earth and more than 5bn people with phones, and the last billion are necessarily the slowest and hardest to reach. Phone sales are a function of the install base and the replacement rate - the install base hasn’t got much more growth and the replacement rate is also starting to lengthen (or at least not shorten). So phone sales will slow. Then, most phone sales now are already smartphones (as seen in the chart above), so the conversion of phone sales to smartphone sales also hasn’t got much further to grow. The smartphone install base does have a lot of room to grow, but that's a function of replacement at close to existing volumes, and even that will be largely done in a few more years. Hence: smartphone sales growth is slowing down.

On one level this is just classic saturation - no industry can grow forever. But what happens next?

At the level of the consumer internet, it’s been clear for some time that Apple and Google won the platform war and that the important questions have moved up the stack - how far can Google and Facebook capture attention and intent, what other interaction models will emerge, how far Android and iOS can shape interaction and consumer behaviour, and so on.

For the hardware companies themselves, though (and that includes Apple), when you’re selling to everyone on earth (something the tech industry has never really done before), what do you do next? TV, once thought of as the next phase after PCs, turned to be an accessory to smartphones, and so are watches and (to some extent) even tablets. VR and AR are some time away with unclear market size, though I think AR could in principle be the next ecosystem after the smartphone.

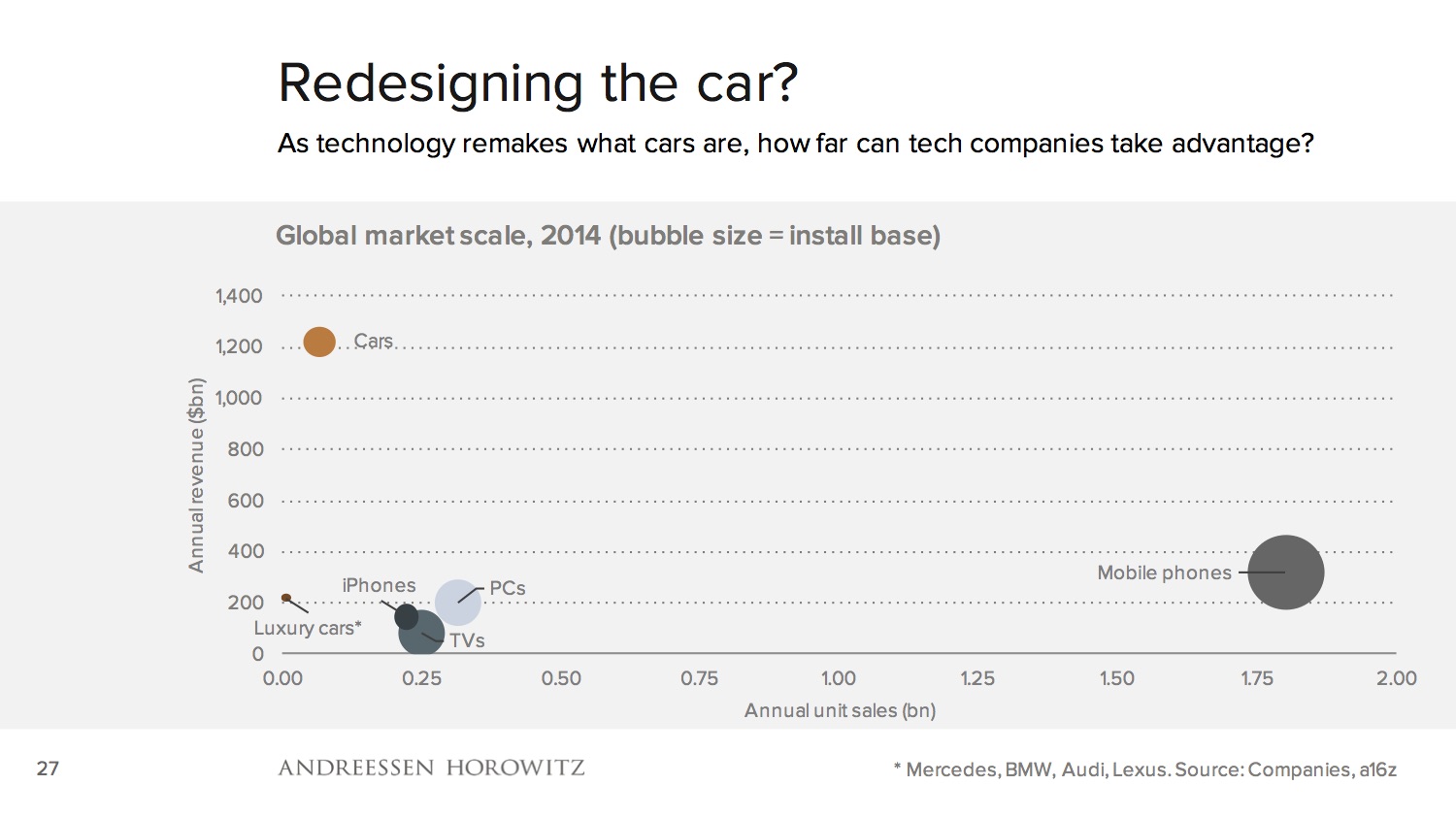

The obvious next market is cars, which in aggregate are much larger in revenue terms, and where a large part of the supply chain will be fundamentally remade by the shift to electric and (in due course) to autonomy. Cars are a Big Deal for the tech industry.

But it’s also interesting to think about the phone market itself, which isn’t going away any time soon (though AR may affect that in the next decade).

I spent some time chatting to Condor at MWC this spring. It's a subsidiary of an Algerian family-owned conglomerate, which began in the cement business and expanded into white goods - fridges and washing machines - and then televisions ('brown goods'). It built a nation-wide network of 150 stores to support that business. Then it got into the phone business, and last year it sold 3m phones, of which 2.8m were Android smartphones. The best-selling model retails for $80. It expects to reach sales of $1bn this year, and has around a third of the Algerian market.

Condor is possible because mobile phone technology became something that you could buy off the shelf - if you can make a TV, you can make a mobile phone or a smartphone, without needing deep understanding of how cellular technology works anymore, or writing your own OS. In parallel, the manufacturing base of the industry moved from factories you own yourselves to outsourced contracting. So, you can make phones, or get someone else to make them for you, or some combination of the two, with much lower barriers to entry. And if you come from the cement business, your idea of a great margin looks rather different to Sony's.

However, there's a big difference between making a phone and selling it. It’s all very well to put it in a shipping container in Shenzhen, but what happens after that? A lot of Apple's sales growth since 2007 has actually been about expanding distribution through mobile operators (which sell far more iPhones than Apple retail does), with the really big additions being Verizon Wireless and China Mobile. Indeed, the fact that it has now signed up all the operators that matter is one reason sales growth has slowed. In parallel, distribution was a big part of the Samsung story. It has effectively cloned Nokia: it offers every technology, frequency and specification, at every price point, for every operator, through every sales channel, and spends billions of dollars on sales and distribution to support that, of which a very large part will be sales commissions.

That is, with the tech available off the shelf, the barrier to entry has moved from the creation and manufacture of the phones themselves to sales, distribution, marketing and support, and a lot of the innovation in the handset business now is around how to address that. Which part of the value chain do you start from and try to leverage, and which parts you outsource? Someone has to make it, someone has to import it, someone has to put into shops, or market it for online sales, and (especially in developed markets) someone has to provide support if you smash the screen. But all of those are being disassembled and reassembled in different combinations.

Hence, at one end of the spectrum are Chinese companies that are just looking for distribution deals overseas, and will sell you a few thousand or tens of thousand with the brand of your choice printed on the back, and what happens after the shipping container (or suitcase) leaves Shenzhen is up to you. The next step along are those trying to create a brand of their own, often in parallel with selling phones under other people's brands. So I've met several companies that have a slick new consumer brand of their own with nicely designed handsets and a decent Android skin, and are thinking about how to take that abroad - what that sales and distribution might look like, and where it should be. One interesting illustration of this is Wiko, which has a double-digit share of the French market and is expanding in south-east Asia. The back of the phone says ‘Designed in France, Assembled in China’, but in fact Wiko seems to be majority owned by a Chinese company, Shenzhen Tinno Mobile Technology Company Ltd.

Sitting right next to Wiko are ever more companies starting from the other end - building brand, distribution and marketing locally, adding some design, and outsourcing the manufacturing. Wiley Fox in the UK comes from people with a background in mobile operators, selling a premium design at a mid-range price with a lightly skinned version of Android. BQ in Spain originates in ereaders, amongst other things. Blu in Latin America has built a huge business on distribution. And of course Google sells its own ’Nexus’ line, using a rarely-encountered custom build of Android and adding a small amount of marketing and distribution.

As the price for a good Android experience moves from $600 to $150 or $250, these companies can increasingly pass up operator subsidies, with burdens of inventory etc. that this imposes, and move straight to selling unsubsidised and online. The poster-child for this model is of course Xiaomi, which has pioneered an online-only flash sales model, backed by an attempt to build a passionate community around the brand and software experience. This has worked well in China but it's not clear how well it can be made to work elsewhere, and whether it can be built once and scaled globally or whether you need to do it one country at a time from scratch.

Then, coming from the other end of the spectrum, mobile operators are increasing buying in a selection of low-end smartphones than they sell (generally unsubsidised on prepay) under their own brand. Sometimes these have operator apps preloaded (if they've not given up on that yet), sometimes not. One could argue that the value being added here is really only distribution, and so one might see other companies with distribution getting into this, such as mass-market retailers. Some of these have already experimented with Android tablets, with mixed results (as of course they did with MVNOs).

This is all rather like the PC clone market of the 1980s - hundreds of undifferentiated companies fighting it out to sell commodity computers built with commodity components running a commodity operating system (though those companies mainly made the PCs themselves, where many phone brands do not). That world in due course led to companies like Dell - people who embraced the volume, low-margin commodity model and found an angle of their own. We’re starting to see equivalent model-creation now.