Featured

Newsletter

July 2026

What mattered in tech this week?

What happened in tech that mattered, and what did it mean? Once a week, I send an email newsletter to close to 200,000 people – I pick out the changes and ideas you don’t want to miss in all the noise, and give them context and analysis.

SUBSCRIBE

May 2026

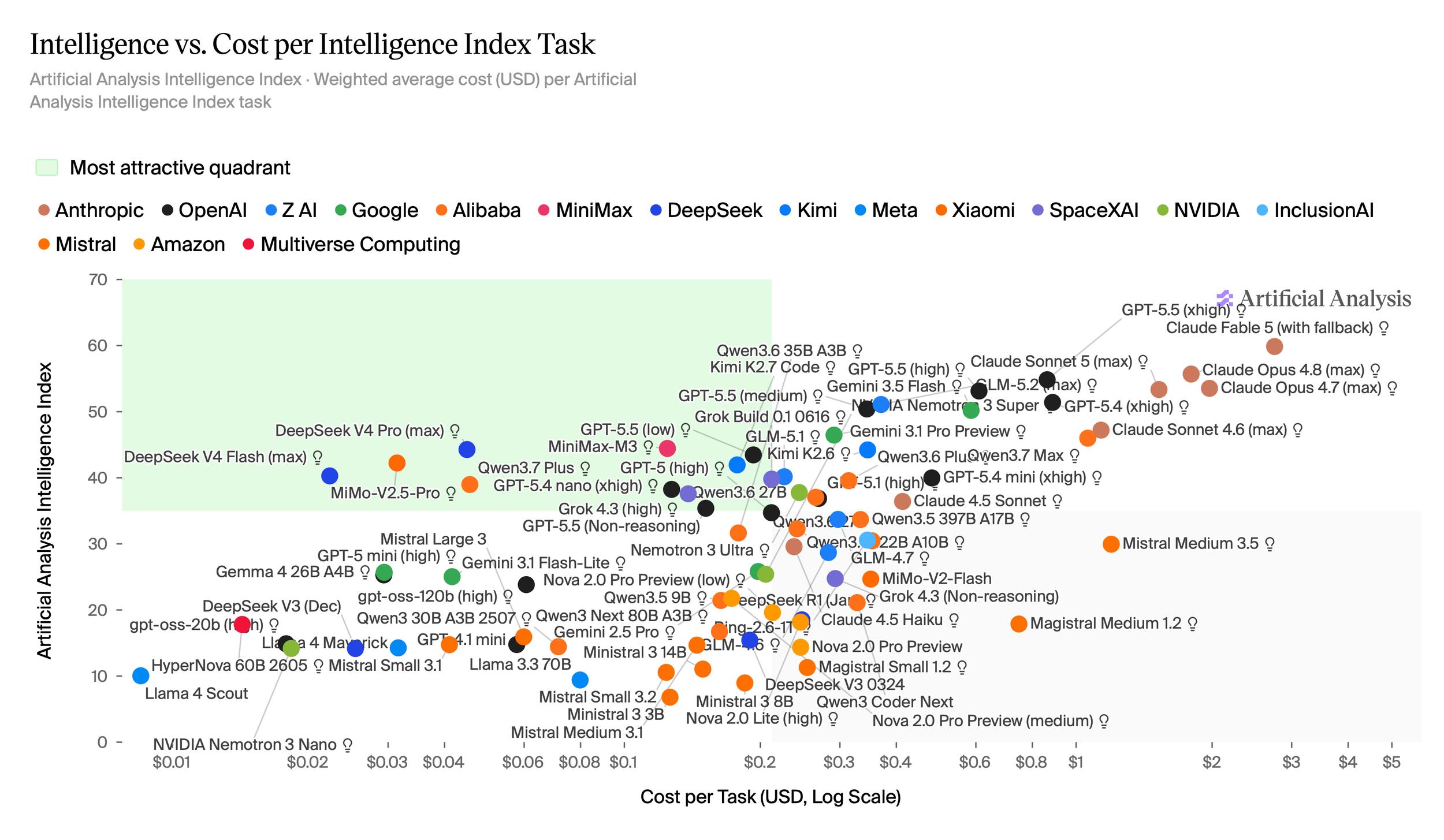

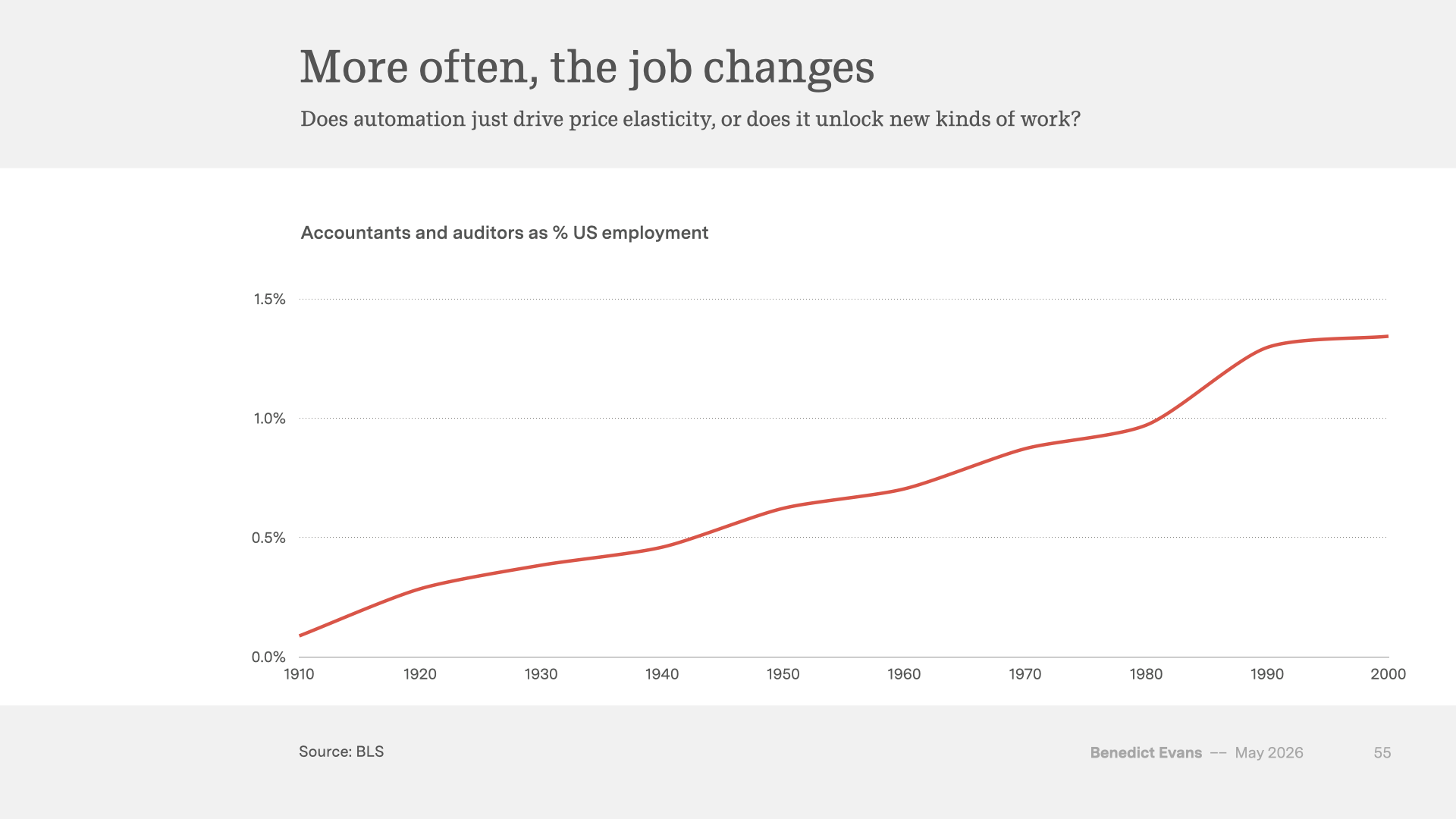

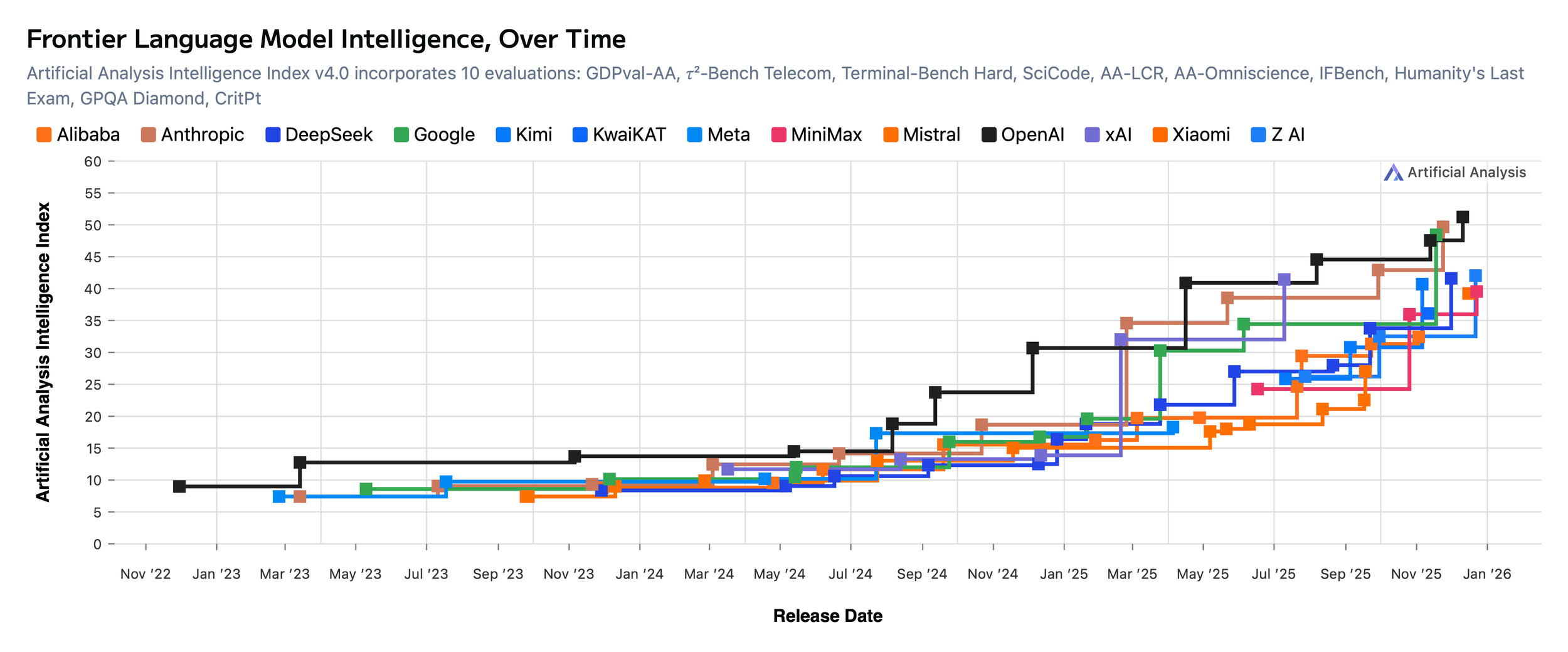

AI eats the world

Twice a year, I produce a big presentation exploring macro and strategic trends in the tech industry. For Spring 2026, ‘AI eats the world’.

2026